Originally published on Medium.com

The investment industry has a hidden secret.

While retail investors obsess over annual returns, professional fund managers use completely different metrics to evaluate performance. They know something most individual investors don’t: absolute returns are meaningless without context.

Consider this real example from recent market history. During the dot-com boom of the late 1990s, many technology-focused mutual funds posted spectacular 40-50% annual returns. Investors poured money in, chasing these impressive numbers.

Then reality hit.

From 2000 to 2002, the NASDAQ fell 78%. Many of those “high-performing” funds lost 60-80% of their value and took over a decade to recover. Meanwhile, boring balanced funds recovered their losses much quicker.

This is is why professionals focus on risk-adjusted returns—they measure how much profit you generate for each unit of risk you take.

This article will teach you the four essential metrics that separate amateur speculators from serious wealth builders. You’ll learn how modern hedging instruments can protect your portfolio during market crashes. Most importantly, you’ll discover why the tortoise really does beat the hare in long-term wealth creation.

The Fatal Flaw in How Most People Measure Success

Here’s the problem with focusing solely on returns.

Investment performance without risk context is like judging a car by its top speed while ignoring its brakes, handling, and safety features. A vehicle that reaches 200 mph is impressive until you need to navigate a corner or stop suddenly.

The same principle applies to your portfolio.

Academic research consistently shows that investors who chase the highest returns often end up with the worst long-term outcomes. A 2019 study by Dalbar found that while the S&P 500 returned 10.16% annually over 20 years, the average equity investor earned only 5.04% due to poor timing decisions driven by emotional reactions to volatility.

The solution lies in understanding risk-adjusted performance metrics.

These tools help you evaluate investments based on the relationship between returns and the risks taken to achieve them. They answer the crucial question: “Am I being adequately compensated for the risk I’m taking?”

The Four Pillars of Professional Investment Analysis

Professional portfolio managers rely on four key metrics to evaluate true performance. Each provides a different lens for understanding the risk-return relationship.

1. Maximum Drawdown: The Reality Check

Maximum Drawdown (MDD) measures the largest peak-to-trough decline in portfolio value before a new peak is reached. If your portfolio grew from $100,000 to $150,000, then fell to $105,000 before recovering, your maximum drawdown would be 30%.

Why this matters more than you think:

Behavioral finance research shows that most investors cannot psychologically handle drawdowns exceeding 20-25% without making emotional decisions that damage long-term returns. The 2008 financial crisis provided a real-world test of this principle—many investors who experienced 40-50% drawdowns, panic-sold near market bottoms and missed the subsequent recovery.

Professional application: Institutional investors often use maximum drawdown as a primary constraint in portfolio construction, preferring strategies that limit worst-case losses even if it means accepting lower potential returns.

2. The Sharpe Ratio: Wall Street’s Gold Standard

Developed by Nobel laureate William F. Sharpe, this ratio measures excess return per unit of total volatility. The formula divides the investment’s return above the risk-free rate by its standard deviation.

Formula: (Investment Return - Risk-Free Rate) / Standard Deviation

Interpretation guidelines:

• Sharpe ratio above 1.0: Good risk-adjusted performance

• Sharpe ratio above 2.0: Excellent performance (rare)

• Sharpe ratio below 0.5: Poor risk-adjusted returns

The limitation: Sharpe ratio penalizes all volatility equally, treating upside volatility (gains) the same as downside volatility (losses). This creates a blind spot for strategies that deliver asymmetric returns.

3. The Sortino Ratio: The Smarter Sharpe

The Sortino Ratio addresses Sharpe’s primary weakness by focusing only on downside deviation—the volatility of negative returns. This provides a more realistic assessment since investors typically don’t mind “volatility” that comes from gains.

Formula: (Investment Return - Risk-Free Rate) / Downside Deviation

Why it matters: Two portfolios might have identical Sharpe ratios, but the one with the higher Sortino ratio achieves its returns with fewer and less severe negative periods. This translates to better investor experience and higher likelihood of sticking with the strategy long-term.

Academic validation: Research published in the Journal of Portfolio Management found that Sortino ratios better predict future risk-adjusted performance than Sharpe ratios, particularly for strategies with asymmetric return distributions.

4. The Calmar Ratio: The Disaster Recovery Test

The Calmar Ratio compares annualized return to maximum drawdown, providing insight into how efficiently an investment recovers from its worst losses.

Formula: (Annualized Return - Risk-Free Rate) / Maximum Drawdown

Professional benchmark: Hedge funds and managed futures strategies often target Calmar ratios above 1.0, indicating that annual returns exceed the worst single loss experienced.

Historical perspective: During the 2008 crisis, strategies with high Calmar ratios recovered much faster than those with poor ratios, even when absolute returns were similar.

Case Study: Why Risk-Adjusted Thinking Matters

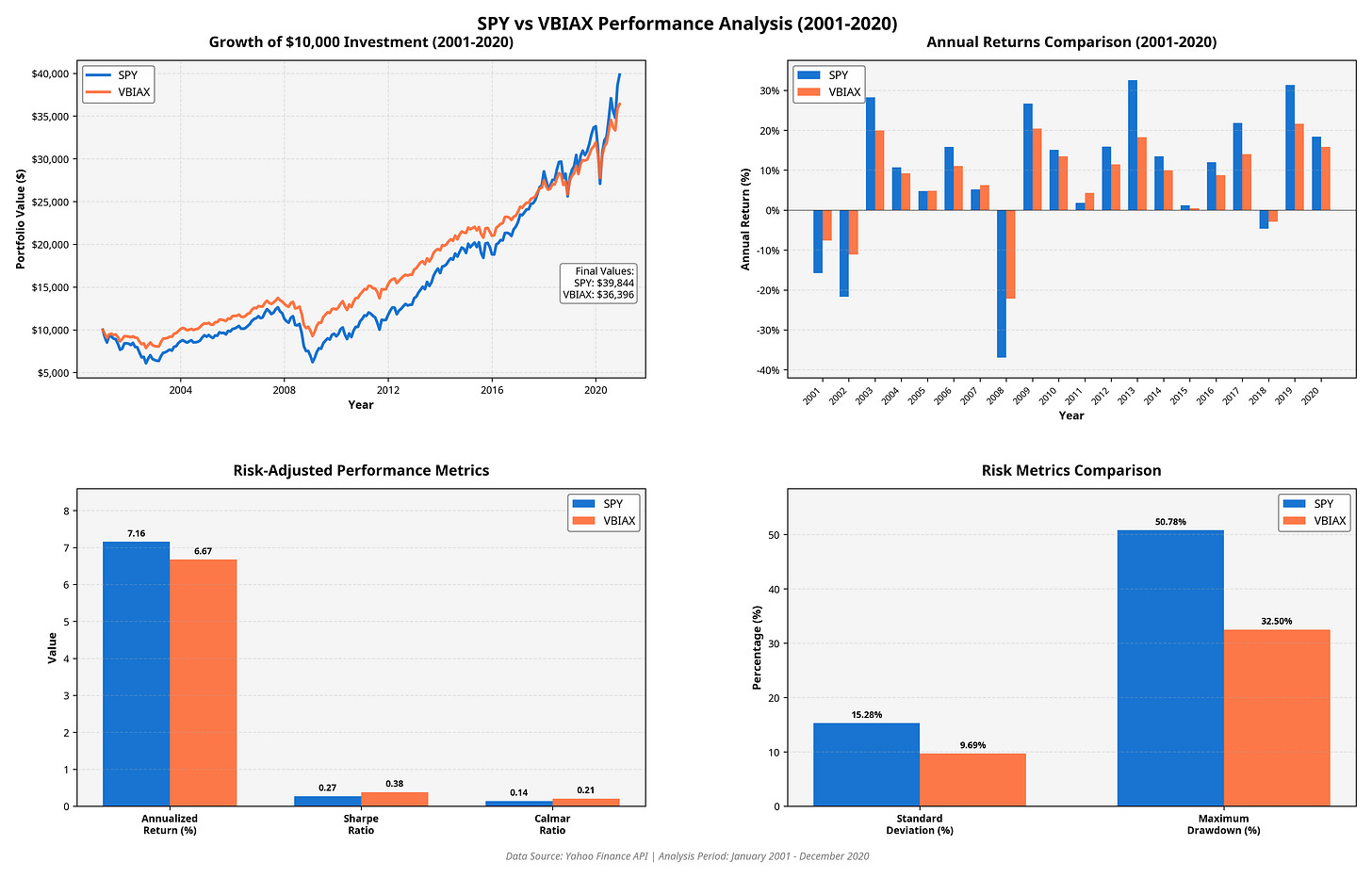

Let’s examine two real investment approaches using historical data to illustrate these concepts. Strategy A representing S&P 500, while Strategy B representing a simple diversified portfolio of 60% stocks and 40% bonds.

Strategy A: Broad Market Portfolio (S&P 500 - SPY)

• Period: 2001-2020 (20 years)

• Annualized Return: 7.16%

• Standard Deviation: 15.28%

• Maximum Drawdown: -50.78%

• Sharpe Ratio: 0.27

• Calmar Ratio: 0.14

Strategy B: Simple Diversified Portfolio (Vanguard Balanced Index Fund - VBIAX)

• Period: 2001-2020 (20 years)

• Annualized Return: 6.67%

• Standard Deviation: 9.69%

• Maximum Drawdown: -32.50%

• Sharpe Ratio: 0.38

• Calmar Ratio: 0.21

The analysis reveals a counterintuitive truth: Despite Strategy A’s higher absolute returns, Strategy B delivered superior risk-adjusted performance across all metrics. More importantly, Strategy B’s journey was psychologically more sustainable, while Strategy A’s 73% drawdown was simply nerve-racking for most investors.

This is where modern portfolio analysis tools become invaluable. Platforms like Zehnlabs calculate these sophisticated metrics (among others) for several strategies, providing institutional-grade analysis that was previously available only to institutional investors and private hedge fund managers. Instead of manually computing complex ratios, investors can focus on making informed decisions based on comprehensive risk-adjusted data.

Advanced Portfolio Protection: Beyond Traditional Diversification

Understanding risk is the first step. Managing it proactively is where sophisticated investors separate themselves from the crowd.

Traditional diversification means spreading your money across different types of investments—like stocks, bonds, and commodities. The idea is that when one investment goes down, another might go up, helping to balance out your overall portfolio. This approach typically provides protection during normal market conditions.

However, traditional diversification has a critical weakness: it often fails when you need it most. During major market crises—like the 2008 financial crisis or the 2020 COVID crash—different asset classes tend to move in the same direction—downward. In technical terms, their “correlation” spikes toward 1.0, meaning they’re all falling together instead of balancing each other out.

When this happens, your “diversified” portfolio might drop significantly because everything is declining at once. This is why modern portfolio protection requires more dynamic approaches—strategies that actively adjust to changing market conditions rather than simply holding a static mix of different assets.

Volatility-Based Hedging: Profiting from Market Fear

The CBOE Volatility Index (VIX) measures implied volatility in S&P 500 options, effectively quantifying market fear and uncertainty. Historical analysis shows strong negative correlation between VIX levels and equity returns, making volatility-based instruments powerful hedging tools.

Key volatility instruments:

• VIXY (ProShares VIX Short-Term Futures ETF): Provides 1x exposure to short-term VIX futures

• UVXY (ProShares Ultra VIX Short-Term Futures ETF): Offers leveraged exposure for more aggressive hedging

Historical performance during crises:

• March 2020 COVID crash: UVXY gained over 1,000% while S&P 500 fell 34%

• February 2018 “Volmageddon”: VIXY surged 90% during market correction

Inverse ETFs: Simplified Downside Protection

Inverse ETFs provide exposure opposite to their underlying index without the complexity of short-selling or options strategies. When the S&P 500 declines 1%, an inverse S&P 500 ETF should gain approximately 1%.

Popular inverse instruments:

• SH (ProShares Short S&P500): -1x daily performance of S&P 500

• PSQ (ProShares Short QQQ): -1x daily performance of NASDAQ 100

Advantages over direct short-selling:

• No margin requirements or borrowing costs

• No risk of unlimited losses

• Professional management of underlying positions

• Easy liquidity through normal brokerage accounts

Critical Implementation Considerations:

Volatility and inverse ETFs carry high levels of risk and are not suitable for most retail investors. These products require proper risk management and are best suited for experienced, sophisticated investors. While they can be indispensable tools for the right investors, they demand expertise to use effectively.

Common Implementation Mistakes and How to Avoid Them

Even sophisticated investors often make critical errors when implementing risk-adjusted strategies.

Over-Optimization and Curve Fitting

The mistake: Designing strategies that perform favorably on historical data but fail in real markets due to over-fitting to past patterns.

The solution: Focus on robust strategies that work across different market environments rather than those optimized for specific historical periods. Use out-of-sample testing and walk-forward analysis to validate approaches.

Ignoring Transaction Costs and Market Impact

The mistake: Implementing strategies that look attractive on paper but become unprofitable after accounting for real-world trading costs.

Hidden costs include:

• Bid-ask spreads

• Commissions and regulatory fees

• Tax implications of taxable events

• Market impact from large orders

The solution: Factor all costs into strategy evaluation. Quite often a theoretically inferior approach with lower implementation costs produces better net results.

Correlation Breakdown During Crises

The mistake: Relying on hedges that work during normal markets but fail exactly when protection is most needed.

Historical example: During the 2008 crisis, many “diversified” portfolios crashed together as correlations spiked to near 1.0. Traditional diversification provided little protection when it was most needed.

The solution: Use multiple hedge types that respond to different stress scenarios. Combine systematic hedges (like volatility ETFs) with fundamental hedges (like Treasury bonds) and tactical hedges (like inverse ETFs).

Emotional Override of Systematic Approaches

The mistake: Abandoning disciplined approaches during periods of stress or euphoria.

Behavioral research: Studies show that even sophisticated investors often override their own systematic rules during extreme market conditions, typically buying high during bubbles and selling low during crashes.

The solution: Implement systematic rules with specific triggers and commit to following them regardless of market sentiment. Use position sizing and gradual implementation to reduce the temptation to make large, emotional adjustments.

The Psychology of Risk-Adjusted Investing

Understanding the behavioral aspects of risk management is as important as the mathematical components.

Loss Aversion and Prospect Theory

Nobel Prize-winning research by Daniel Kahneman and Amos Tversky demonstrated that people feel losses approximately twice as intensely as equivalent gains. This psychological asymmetry explains why:

Investors often sell winners too early and hold losers too long. The pain of realizing a loss feels worse than the pleasure of taking a profit, leading to suboptimal portfolio management.

High-volatility strategies often underperform in practice. Even when mathematically superior, strategies with large drawdowns trigger loss aversion responses that cause investors to abandon them at the worst possible times.

Risk-adjusted approaches align with human psychology. By focusing on smoother return patterns, these strategies work with human nature rather than against it.

The Paradox of Choice and Decision Fatigue

Research shows that too many options can lead to decision paralysis and poor choices. In investing, this manifests as:

Analysis paralysis: Investors who spend excessive time researching perfect strategies often delay implementation and miss opportunities.

Strategy hopping: Constantly switching between approaches based on recent performance rather than sticking with sound long-term strategies.

The solution: Focus on a small number of well-understood, robust strategies rather than trying to optimize every detail. Simplicity often beats complexity in real-world implementation.

Social Proof and Herding Behavior

Humans have strong tendencies to follow crowd behavior, especially during uncertain periods. In markets, this creates:

Bubble formation: When everyone is buying, prices can become disconnected from fundamental value.

Panic selling: During crashes, the urge to follow others can override rational analysis.

Risk-adjusted frameworks provide objective anchors that help investors resist emotional crowd-following behaviors by focusing on quantitative metrics rather than market sentiment.

Conclusion: The Investor You’re Becoming

The shift from return-focused to risk-adjusted thinking represents a fundamental evolution in investment sophistication.

While others chase the latest market trends or hot investment themes, you’ll be building antifragile wealth designed to compound steadily over time. While they experience emotional rollercoasters that lead to poor timing decisions, you’ll maintain the psychological equilibrium necessary for long-term success.

This transformation doesn’t happen overnight. It requires patience, discipline, and continuous learning. But the compound benefits of risk-adjusted thinking extend far beyond portfolio returns—they include better sleep, reduced stress, and the confidence that comes from having a systematic approach to uncertainty.

The tools and knowledge exist today to implement institutional-quality risk management in individual portfolios. Platforms like Zehnlabs have democratized access to sophisticated trading strategies, previously only available to private hedge funds and institutional traders. The question isn’t whether you can afford to implement these strategies—it’s whether you can afford not to.

The market will continue to present opportunities and challenges. Your risk-adjusted approach will help you navigate both with confidence and clarity.

References

[1] Dalbar, Inc. “Quantitative Analysis of Investor Behavior (QAIB) 2019.” https://www.dalbar.com/QAIB/Index

[2] Investopedia. “Maximum Drawdown (MDD).” https://www.investopedia.com/terms/m/maximum-drawdown-mdd.asp

[3] Investopedia. “Risk-Adjusted Return.” https://www.investopedia.com/terms/r/riskadjustedreturn.asp

[4] Fowls, Will. “Sharpe Ratio, Sortino Ratio, and Calmar Ratio.” Medium. https://medium.com/@williamchristianfowls/sharpe-ratio-sortino-ratio-and-calmar-ratio-4738a3574fdb

[5] Wall Street Prep. “Risk-Adjusted Return.” https://www.wallstreetprep.com/knowledge/risk-adjusted-return/

[6] Kavout. “How to Use Volatility ETFs for Hedging and Opportunity in Uncertain Markets.” https://www.kavout.com/market-lens/how-to-use-volatility-et-fs-for-hedging-and-opportunity-in-uncertain-markets

[7] Investopedia. “Inverse ETFs Can Lift a Falling Portfolio.” https://www.investopedia.com/articles/mutualfund/07/inverse-etfs.asp

[8] Kahneman, Daniel, and Amos Tversky. “Prospect Theory: An Analysis of Decision under Risk.” Econometrica, vol. 47, no. 2, 1979, pp. 263-291.

Author Bio:

Faisal Haroon is the founder of Zehnlabs, providing tactical asset allocation strategies for active investors. After analyzing thousands of trading strategies and portfolios, he developed systematic approaches to alpha creation and risk management based on quantitative research. While he advocates passive indexing for most investors, Zehnlabs serves those seeking data-driven, actively managed portfolio strategies.

Conflict of Interest Disclosure:

The author operates Zehnlabs, which offers paid tactical asset allocation strategies. This potential conflict of interest is disclosed so readers can evaluate the article’s perspective accordingly.

Learn more at zehnlabs.com/fintech